Enterprise Risk Management that brings clarity to complexity

Trusted by hundreds of clients globally

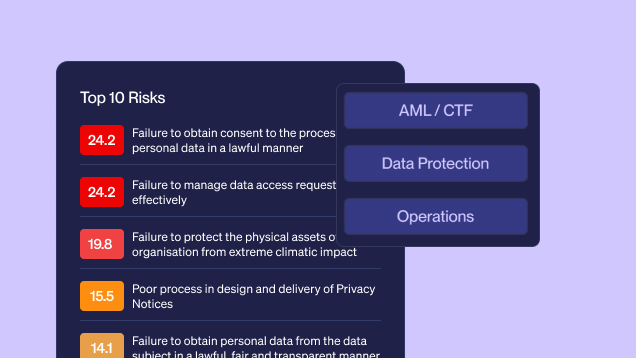

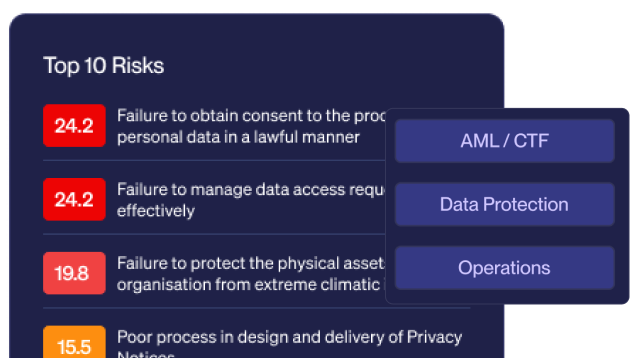

Master enterprise-wide risk

Gain complete visibility across your risk universe with clarity, consistency and real-time intelligence.

Report at the click of a button

Generate tailored reports on risks, controls and more with a single click.

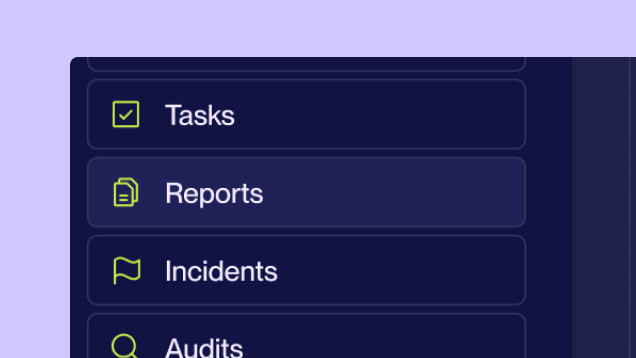

Track tasks and accountability

Assign and track remediation actions across your team ensuring nothing slips through the cracks.

Streamline internal controls

Use pre-populated libraries to map risks to controls, assign ownership and track control testing.

Configure without coding

Tailor structures and alerts to your exact needs using powerful no-code configuration options.

Customer Testimonials

calQrisk is essential for any organisation that needs a risk management / compliance solution that will evolve with their business and provide them with the essential ingredients that will allow them manage their risks on an on-going basis.

calQrisk was the obvious choice for enhancing our governance processes. From the outset, the solution has delivered immediate time savings and has significantly improved the efficiency and transparency of our operations. The onboarding process was smooth making the transition seamless.

We found calQrisk extremely helpful inthe preparation of our Risk Register. It prompted us to put into place all the relevant policies and procedures that we needed.

The calQrisk software has become a critical element of the Housing Agency’s Risk Management Framework. It has become a vital tool used by all members of staff, to ensure the effective monitoring of risks against our strategic objectives and the regulatory compliance of our organisation.